Retirement income: A new lens

Picture a client in retirement, and you’ll see many different images – each with unique characteristics. While they differ from working clients and from one another, retired clients share one common requirement: income. In a landscape shaped by regulatory shifts and an unpredictable economic environment, retirement planning is evolving. Fresh perspectives are emerging on the techniques best suited to meet the diverse needs of clients in retirement. Just as a photographer adjusts their lens and exposure for different results, financial strategies must be tailored to capture the right focus for each individual. The challenge is crafting an approach that ensures stable, sustainable income throughout retirement, regardless of the client profile.

reframing retirement

infographic Natural income in sharp focus

retirement reimagined

Zooming in on investing in retirement

creating picture-perfect retirements

Fresh perspectives

on retirement advice

Meet the income earner

watch

read

Contact

Explore

Natural income in sharp focus

Watch

Reframing retirement

Retirement reimagined

Read

Is it time to reframe your thinking about natural income?

Contact us

Creating picture-perfect retirements

New research sheds light on how advisers are reacting to the altering retirement advice landscape

New research from BNY Investments and NextWealth – titled Retirement Advice in the UK: Time for Change? – comes at an important time in the assessment of approaches to retirement advice. Regulatory scrutiny and tax changes are altering the retirement advice landscape and sharpening the focus on the investment strategies and products advisers use for clients in decumulation. The FCA reported its findings of the long-awaited thematic review of retirement income advice in March 2024 and stressed the importance of acting on its findings in its portfolio letter to CEOs of financial advice businesses in October last year. Later that month, the first Budget since the Labour Party came to power in July also had significant implications for retirement planning – not least the inclusion of unused pensions in the inheritance tax regime. With retirement income advice expected to be a primary focus for regulatory activity over the next two years and tax changes being seen by advisers as the main driver of growing demand for their services, financial advice firms must be adaptable and proactive to meet these challenges. In words and charts, we zoom in on the findings of the NextWealth report to reveal how advisers are changing their retirement offerings and identify where retirement advice needs to be adapted for the evolving market environment. The report gathered insights from 208 financial advisers and 254 consumers of retirement advice, aged 55 or over, and with a minimum of £100,000 of investable assets.

zooming in on

investing in retirement

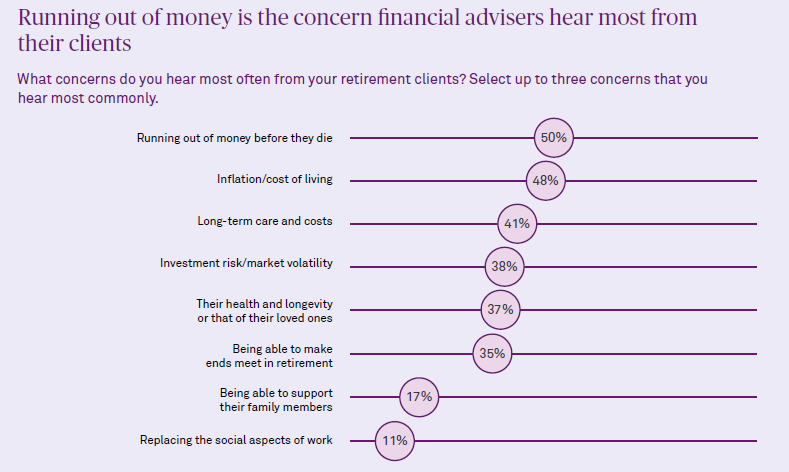

The research identifies the key concerns clients express to their advisers about retirement. Chief among these is the fear of running out of money.

Most advised clients (97%) have at least some confidence they won’t outlive their assets but are slightly less assured their savings will enable them to maintain their standard of living in retirement or be sufficient to keep pace with the cost of living.

Client concerns

As a result of the retirement income advice review, financial advisers plan to increase their use of cashflow planning tools.

It is important to recognise, however, that the output of cashflow modelling is only as good as the assumptions used to create the model. A key recommendation from the FCA’s thematic review is that firms must be able to demonstrate an understanding of the standard assumptions used to create the model and clearly explain them to clients. Cash buffers are used by many advisers (84%) to reduce sequencing risk and provide security of income for clients, particularly during uncertain and volatile times. The size of these buffers is increasing, with more than one in four advisers now allocating three to four years of income to cash.

Outsourcing is also becoming more commonplace as advisers enlist the investment expertise of discretionary fund managers, multi-managers and multi-asset fund managers. The Consumer Duty appears to be driving this transition from in-house to externally managed portfolios for retirement clients.

Firms expect to increase their use of outsourced model portfolios and multi-asset funds the most over the next three years.

The report also gauged the popularity of three main approaches to structuring portfolios for clients seeking a regular income. It identified a growing trend towards income-driven and bucket approaches. These methods help to manage sequencing risk and provide a more predictable income stream. Total return approach Fuelled by the era of rock-bottom interest rates and low bond yields, investing for total return with income payments funded by selling investments has become the most favoured option among advisers, with 51% using it all or most of the time. This approach allows for flexibility in generating income through capital gains and dividends but exposes investors to unsustainable yields and having to sell investments into a falling marke Income-driven approach Higher interest rates and bond yields make an income-driven approach more viable, and the approach is now used by 34% of advisers all or most of the time. Income payments are derived from the income generated from investments and can be topped up by selling investments, thereby providing a more predictable income stream and mitigating sequencing risk. Bucket approach A bucket or time-segmented approach, whereby the portfolio is split into cash for short-term income needs, intermediate assets for medium-term needs and growth assets for longer-term needs, is used by 41% of advisers all or most of the time. This approach offers a systematic way to manage investments aligned with specific client needs, providing stability and reducing the impact of market volatility.

Approaches to structuring client portfolios

In the coming year, about one-fifth of financial advisers intend to make greater use of bucket and income-driven approaches. The variability of income deters just over one-third of advisers from using a natural income approach, but this can be overcome by ‘managed income’ funds, which seek to generate a more stable level of monthly income and ease the planning process.

Increased confidence

The report’s findings give firms insight into what peers are doing and allows them to benchmark their own approach. While advisers have plenty to digest as they seek to build scalable, repeatable and compliant retirement advice processes, they can feel satisfied with the service they already provide clients. The report shows that retirement advice is hugely valued by those who receive it. Overall, clients reported a high level of satisfaction from working with an adviser and increased confidence in achieving their retirement goals.

Running out of money before they die

Inflation/cost of living

Long-term care and costs

Investment risk/market volatility

Their health and longevity or that of their loved ones

Being able to make ends meet in retirement

Being able to support their family members

Replacing the social aspects of work

50%

48%

41%

38%

37%

35%

17%

11%

Use a cashflow/scenario modelling tool

Use a fixed rate or range (e.g. the 4% rule)

Assess based on annuity rates

Recommend clients only take portfolio income

Use the Government Actuarial Department rate

35

27

21

11

7

6

41

17

14

18

31

28

16

5

15

30

29

9

10

19

%

All of the time

Most of the time

Some of the time

Rarely

Never

Making sure my money lasts as long as I need it to

Very confident

Moderately confident

46

37

2

39

34

20

33

32

22

24

Maintaining the same standard of living as before retirement

Keeping up with changes in the cost of living

Ensuring I can withstand periods of market and economic uncertainty

Somewhat confident

Not confident at all

Don't know/ prefer not to say

40

Maintaining my health and longevity or that of my loved ones

Preparing for long-term care and the associated costs

12

Supporting family members financially

Several retirement planning strategies are prevalent among advisers seeking to address clients’ concerns and ensure income needs are met. Cashflow modelling is the primary method used to engage clients in a detailed conversation about their sources of income and how to create an income for life.

Retirement planning and investment strategies

Cashflow planning

Significantly increase

Somewhat increase

13

25

3

8

57

Stochastic/Scenario modelling

Risk profiling

Slight increase

No change

Don't know

N/A

Typically allocate 1-2 years of income to cash

2024

2023

49

2019

54

58

Typically allocate 3-4 years of income to cash

26

Tend to allocate more than 4 years income to cash

Allocate a fixed percentage of the portfolio cash

Other - please specify

0

4

Don't use cash buffers

Smoothed (with profits) multi-asset funds (e.g. Pru Fund)

2020

Bespoke portfolio outsourced to a discretionary investment manager

Bespoke portfolio managed inhouse

Model portfolios outsourced to a discretionary investment manager

Model portfolios managed inhouse

Multi-asset or multi-manager funds

2018

2021

Increase significantly

Increase a little

64

1

60

Ramain the same

Decrease a little

Dicrease significantly

Model portfolios managed in-house

59

Single strategy funds

Bespoke portfolio managed in-house

Significantly improves confidence

14%

33%

Somewhat improves confidence

53%

No impact on confidence

39%

47%

51%

28%

25%

22%

34%

31%

Total return approach (i.e. portfolio designed to deliver returns with income generated through selling units/shares)

Income driven approach (i.e. portfolio designed to generate natural income with payments possibly supplemented by capital withdrawals from selling units/shares)

'Bucket' approach (i.e. portfolio divided between cash, intermediate and growth assets) with income payments typically funded from cash holdings

Adviser responses

Consumer responses

KEY FOR CHARTS

15%

12%

21%

29%

16%

24%

27%

23%

20%

30%

44%

40%

42%

46%

56%

49%

Focus on delivering predictable and stable income

Jennifer Hill

Investment writer

The Covid-19 pandemic reshaped not only how we approach work but how we view retirement. Flexible work patterns have allowed clients to view their future through a new lens: retirement is no longer an abrupt change but a gradual transition. Some question whether they will retire at all. Our roundtable explores how changes in consumer behaviour and significant regulatory shifts are compelling advisers to rethink their approach to meet the evolving needs of clients in decumulation. How essential are risk profiling and cashflow modelling in ensuring retirement strategies remain flexible, sustainable and tailored to individual needs? How are investment strategies being reimagined to align with the new picture of retirement? Watch the video and read the article to gain insights from a diverse range of industry experts: Richard Parkin, head of retirement at BNY Investments; Heather Hopkins, managing director and founder of NextWealth; Sebastian Gladwish, a senior private client adviser at HFMC Wealth; and Adam Field, a certified financial planner at William Highbourne Wealth Management.

Watch Richard Parkin's interview

READ

Change is upon us, according to BNY’s research on retirement advice, and we brought together a range of experts to explain what this spells for the industry.

As people’s picture of retirement and the regulatory landscape change, so too must the retirement advice market. This is why we brought voices from across the industry to discuss new research from BNY Investments and NextWealth, titled Retirement Advice in the UK: Time for Change? They focused on both the use of retirement advice techniques and retirement investment strategies and products.

reimagined

retirement

Advice techniques

Use of retirement advice techniques has been relatively stable in recent years: 78% use cashflow modelling to estimate a client’s income needs year on year (up from 76% in 2023); 65% use a specific attitude-to-risk questionnaire for retirement clients (2023: 52%); 64% undertake scenario analysis using stochastic or other models to assess possible outcomes based on different market conditions (2023: 59%); and 52% use a specific set of fund choices/portfolios for retirement clients (2023: 53%). The role of cashflow modelling and risk profiling in advice suitability is covered by the Financial Conduct Authority’s (FCA) thematic review of retirement income, and the panellists expect to see growing use of these techniques. ‘The number one concern for clients in retirement is running out of money and the best way to help them feel comfortable with their financial position is through cashflow modelling,’ said Heather Hopkins, managing director and founder of NextWealth. ‘The regulator’s been very clear that you cannot deliver retirement advice without cashflow modelling.’ Sebastian Gladwish, a senior private client adviser at HFMC Wealth, regards cashflow planning as ‘essential’, especially since the flexible working patterns that resulted from the Covid-19 pandemic have led many more people to want to phase into retirement. ‘Life changes and you can model different changes throughout one’s life,’ he said. ‘More and more people don’t have a cliff-edge retirement. And the risk that comes with a phased retirement is different and ever-changing. Having an adviser to assess that is vital.’

‘It doesn’t have to be a dry questionnaire of 15 questions that gives an output of one to seven. There are some cool pieces of behavioural software.’

One aspect of assessing risk that emerged from the review is the need for advisers to start thinking about risk and capacity for loss in the context of a client’s income. ‘This isn’t the same as volatility,’ said Richard Parkin, head of retirement at BNY Investments. ‘Inflation poses a huge risk to clients in terms of income sustainability. Capital loss is important, but it goes beyond a straight volatility measure.’ Adam Field, a certified financial planner at William Highbourne Wealth Management, pointed to the benefit of behavioural and emotional questionnaires. ‘It doesn’t have to be a dry questionnaire of 15 questions that gives an output of one to seven,’ he said. ‘There are some cool pieces of behavioural software, to which you can add assets and liabilities, income and expenditure, to get a much fuller report on someone’s risk profile. That forms a fantastic basis for a conversation with a client.’

Adam Field

certified financial planner, William Highbourne Wealth Management

Hopkins questioned the suitability of using the same investment solutions for accumulation and decumulation clients – an approach taken by 48% of survey respondents. ‘There’s a question in the industry as to whether that’s appropriate,’ she said. ‘When advisers are using a different set of choices, it’s often the income option of the same funds. It will be interesting to see how thinking changes on that.’ There was a clear consensus around the table that retirement clients need different investment strategies – and that the right strategy depends on each client. Secure income is a huge focus. The state pension is one aspect of this, coupled with final salary pensions for those fortunate enough to have such entitlement. ‘If a couple has the full state pension, that’s £23,000 of inflation-linked income coming into the house,’ said Field. ‘We’ve also got the tail end of defined benefit schemes. Those two can create a base of inflation-linked income that is essentially protected. You can add on top of that some natural income and perhaps regular-term deposits.’ For those without the luxury of a final salary pension, typically 55 and under, generating an income while preserving the capital base as far as possible means striking a balance between secure income products and investments. Higher interest rates and the lower tax advantage of pensions following Labour’s first budget in 15 years have made annuities more appealing. Around one-third of financial advisers expect to increase their use of annuities over the next three years, according to the report. Gladwish has upped his usage a little but feels annuities might not be the best solution for clients taking a flexible approach to retirement.

Investment strategies

‘Whether it’s secure investment income or annuity income, I’m interested in the idea of how you blend them together.’

Richard Parkin

head of retirement, BNY Investments

Field refers to ‘the jigsaw of retirement’ and sometimes builds a bond ladder for clients with larger portfolios. ‘When someone’s got a large asset base, you can set aside some of it in an investment grade corporate bond or gilt ladder to create income – there’s no volatility if you hold for the duration – then go for growth with the remainder,’ he said. For BNY, creating the stable and growing income stream that many clients seek means taking a multi-asset approach and not overreaching for income. ‘By allocating to alternatives, our Multi-Asset Income fund got through 2022 without having to significantly reduce income, then as bond yields came back, we moved away from alternatives and picked up bonds,’ he said. ‘Being able to vary the asset allocation to manage that income is really important, as is not overreaching for income. You then have the scope to invest in equities for capital growth, and a higher asset base for income.’ Of course, no single investment strategy or product is right for every client – or perhaps any client. ‘Whether it’s investment income or annuity income, I’m interested in the idea of how you blend them together,’ added Parkin. ‘This has always been where the FCA has come from. Post pension freedom, when it said there was a lack of product innovation, I asked what it meant by that, and the answer was that it’s about blending guaranteed or secure income with investment income.’

WATCH

Retirement planning is evolving and BNY Investments is leading the conversation. In this video, Citywire’s Frank Talbot sits down with Richard Parkin, head of retirement at BNY Investments, to understand how advisers can address the challenges brought about by the FCA’s 2024 review of retirement income advice. As the retirement landscape grows increasingly complex, advisers must rethink traditional approaches to ensure suitability, scalability and client understanding. BNY’s research, conducted in partnership with NextWealth, reveals that while advisers anticipate retirement assets will be the lion’s share of their businesses, nearly half foresee regulation impacting the time needed to deliver advice. With advisers grappling with regulatory expectations, rising demand and shifting client needs, Parkin highlights solutions BNY offers to streamline the process. These include innovative client reporting tools, a comprehensive suite of end-client materials and a focus on income-led investment strategies. Whether through income-led or total return strategies, Parkin emphasises the value of structured planning in ensuring stable and growing income for retirees. This is a must-watch for advisers navigating the new retirement era.

‘While advisers anticipate retirement assets will be the lion’s share of their businesses, nearly half foresee regulation impacting the time needed to deliver advice’

Watch Paul Flood's interview

‘Having consistent monthly income with a bonus payment at the end of the year is very much like what people feel when they have a salary’

If there’s one thing Paul Flood appreciates, it’s the benefit of flexibility. The head of mixed-asset investment at Newton Investment Management has invested through several market cycles, expertly tilting assets towards the best opportunities for income and growth at any point in time. Since the inception of the BNY Mellon Multi-Asset Income fund a decade ago, his allocation to bonds has ranged from 12% to 30%. When bonds weren’t working as a source of income or a diversifier, he found real assets a better place to be, having as much as 35% in alternatives and as little as 15%. His objective is to create the regular and consistent income stream that many clients seek, which he delivers through a focus on natural income to avoid risking the capital base needed to generate the income of the future. ‘Having consistent monthly income with a bonus payment at the end of the year is very much like what people feel when they have a salary,’ he said. ‘That helps both individuals, but importantly, their advisers plan better over the longer term.’ Citywire’s head of investment research Frank Talbot caught up with Flood to discover how he helps meet the needs of clients in retirement and the importance of a truly multi-asset approach to income.

Watch the Round Table

creating

picture-perfect

For Matthew Dewsnap, investment director of QuantQual, a Dorset-based portfolio research and consultancy firm, today’s investment environment necessitates ‘thinking differently’. He joined the firm, which supports advisers with outsourced investment research, fund recommendations and comprehensive due diligence reports, in 2022 – the year it was founded – but is experienced enough to remember the years before the global financial crisis. ‘Before the credit crunch, natural income was considered a very strong investment proposition, but the period between 2008 and 2022 created a lot of complacency among advisers and investors in general,’ he says. ‘Back in those days of quantitative easing, low interest rates, low inflation and benign geopolitics, it was easy to find growth – it was everywhere. But today we are living in the opposite world. That means thinking differently. Natural income is coming back on the radar for advisers, and the trend has got much further to run.’ Dewsnap advocates a multi-asset approach to income to spread risk and diversify sources of yield. The BNY Mellon Multi-Asset Income fund, run by Paul Flood, head of mixed assets investment at Newton Investment Management, is one of two core building blocks QuantQual uses in its income solutions range. ‘I have admired Paul Flood throughout my career,’ he says. ‘We have a gold rating on his Multi-Asset Income fund, where he makes extremely good use of investment trusts and manages the income superbly. The days of the star fund manager are over, but Paul is an exceptional leader with a fantastic team.’

In the accumulation phase, retirement planning is about framing the future and capturing a client’s portrait of a perfect retirement. In decumulation, it is about creating the income needed for the client to live their picture-perfect retirement. However, industry viewpoints on the best strategies for retirement income are shifting, as we found out from two consultants.

George Ladds founded Bristol-based financial consultant Money Wise UK in February 2024 to ease the operational burden on small and medium-sized advice firms. Compliance is a key area of focus and Ladds has spent a considerable amount of time digesting the FCA’s retirement income advice review and developing a set of documents designed to fill what he sees as a gap in the market. ‘As a result of the thematic review paper, there’s been an influx of retirement products introduced by asset managers and insurance companies,’ he says. ‘However, while these products address various aspects of retirement, the industry has overlooked one crucial area: the need for a structured retirement planning process.’ The ‘missing link’, according to Ladds, is a centralised retirement proposition – something only 52% of firms have, according to recent research by BNY Investments in partnership with NextWealth. Despite the growing availability of retirement products, Ladds says many financial advice firms lack the tools to integrate a well-defined retirement process into their practice easily. His fully customisable documents include a process document outlining a framework for implementing pension drawdown strategies step by step, a solutions document providing a range of tailored solutions for managing clients’ retirement income, and a retirement questionnaire designed to help planners assess and understand clients’ retirement needs. The FCA’s review should compel advisers to reappraise how they structure portfolios for clients seeking a regular income in retirement, he says. ‘Say, for example, a client has £300,000 and is making £15,000 of capital withdrawals a year. If markets fall 30%, they can no longer take £15,000 and, using the same 5% withdrawal rate, would only get £10,500.

‘Especially in light of the thematic review, you need to consider this carefully. Capital withdrawals do work but such an approach carries risk that may not always be explained to or understood by the client.’ Contrast this with an investment approach that focuses on natural income and generating a stable income stream from a diverse portfolio of assets. Under this scenario, the investments continue to generate income and can be used to top up the cash reserve from which advisers draw down for their clients. ‘Income had bad press during the period of low interest rates and quantitative easing but that is now shifting,’ says Ladds. He likes the approach of the BNY Mellon Multi-Asset Income fund, which has a well-diversified portfolio and a strong track record of producing a regular, consistent income stream. ‘The fund has a yield of around 4%. If markets fall, you are still likely to get that and it will grow over time, meaning you aren’t dipping into capital.’ For Ladds, an important aspect of the strategy is its exposure to a range of alternatives. ‘It’s not your traditional bond/equity split but, instead, offers income diversification,’ he says. ‘The fund’s largest holding is a renewables investment trust, Greencoat UK Wind, which pays a decent yield and is on a sizable discount. This in itself offers significant opportunities.’ He sees an income-driven approach as an increasingly attractive option within a retirement strategy. ‘There are, of course, other options,’ he adds. ‘Ultimately, the decision on the right outcome depends on what the client needs.’

‘Income had bad press during the period of low interest rates and quantitative easing but that is now shifting’

George Ladds

Strategic consultant, Money Wise UK

Every adviser wants to help their clients achieve a picture-perfect retirement, and perspectives on the best way to do so are changing.

Matthew Dewsnap

Investment director, QuantQual

The fact the fund pays monthly income eases the administration process and helps advisers strengthen relationships with clients, who appreciate the smoother journey the fund can provide in retirement, Dewsnap adds. ‘If you can satisfy clients’ income needs through natural income, it puts them in a much stronger position. And if you can’t, it provides a solid start to support the selling down of units. One analogy I like to use is: “Do you want to eat the chicken or collect the eggs?”’ Dewsnap specialises in helping financial advisers with their ongoing investment suitability. He contends that funds like Flood’s stand up well under the scrutiny of the FCA’s consumer duty. ‘There’s been a lot of talk about value but that doesn’t simply mean low cost. The FCA wants advisers to prove value – and this fund offers great value.’ While there are early signs of a revival in natural income, Dewsnap thinks it will require a certain amount of education. ‘Income investing has been out of favour for so long that there are often misunderstandings or gaps in awareness about it. To address this, we’re planning a series of events in 2025 centred on the theme of natural income.’ One misconception he frequently encounters is a focus on the current portfolio yield for an existing investor. ‘This figure is only relevant at the initial point of investment,’ he says. ‘For a natural income strategy to function effectively when an investor begins drawing income, it’s crucial to have the portfolio in place at least a year in advance. This lead time allows the strategy to fully invest and generate the desired income.’ Like all investments, natural income may not be suitable for every client, but Dewsnap and his colleagues at QuantQual have first-hand experience of more advisers realising the benefits of natural income for certain clients. ‘If you haven’t done so yet, now is the time to start thinking about natural income as an addition to your centralised investment and centralised retirement propositions,’ he says.

‘One analogy I like to use is: “Do you want to eat the chicken or collect the eggs?”’

See retirement income through a different lens

retirements

natural income

in sharp focus

Some funds focus on income. Others focus on capital growth. Ours strikes a balance. Aiming for both income and capital growth provides regular income without having to sell investments and allows capital to grow to support investors’ future retirement needs.

Find the right focus

“The level of income is insufficient to meet my clients’ needs”

“An actively managed multi-asset approach can help to generate a good level of income that is stable and growing”

Adviser Ben

Paul Flood

A modern managed income strategy can help to meet the needs of clients in retirement.

1 Retirement Advice in the UK: Time for change?, BNY Investments/NextWealth 2024

Clear the viewfinder

Advisers cite several reasons for not using natural income for decumulation clients1. All of these are debunked when the strategy is carefully constructed and well managed. This is how ‘The income earner’ Paul Flood would respond to four common misconceptions.

Growth focus

income focus

income and growth focus

A multi-asset approach helps to balance income and growth. Higher yielding assets deliver a higher proportion of the income allowing scope for more growth-oriented investments to maintain capital and support income sustainability.

Capture all elements

Asset class

Income yield

Asset allocation

Income contribution

% of total income

Equities

bonds

alternatives

cash

3.6

5.5

8.4

4.5

55

1.3

1.5

0.1

26.7

30.6

2.7

8,000

Annual income (£)

Account value (£)

7,000

6,000

5,000

4,000

3,000

2,000

1,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

Income

Year

A strategy that makes regular and consistent payouts gives clients clarity on their income position. Paying income in 12 equal instalments is analogous to receiving a salary with a balancing payment at the end of the year being like an annual bonus. This stands in sharp contrast to strategies that pay a variable level of income quarterly, biannually or annually.

Steady the shot

Income paid (£)

1,800 1,600 1,400 1,200 1,000 800 600 400 200 0

Fund paying income quarterly, annual income of £5,0001

£980

£1,350

£920

£1,750

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

1,200 1,000 800 600 400 200 0

£800

Income restructured to pay monthly with Christmas bonus1

£350

Source: BNY Investments. This is a hypothetical example provived for illustravive purpose only. 1 Assumes £100,000 in a fund paying 5% per annum.

Since its inception almost a decade ago, the BNY Mellon Multi-Asset Income Fund has delivered stable and growing income while providing scope for capital growth. An initial investment of £100,000 at inception in February 2015 would have generated £44,836 in income and £23,692 in capital growth, resulting in an investment worth £123,692.

Focus on the figures

Initial investment

In income

£ 44,836

investment (30 june 2024)

in capital growth

£3,360

£840

£1,400

£406

£3,543

£794

£3,618

£951

£3,655

£1,029

£3,743

£933

£3,808

£1,071

£3,903

£1,190

£4,342

£949

£4,444

£855

Income paid on the BNY Mellon Multi-Asset Income Fund since inception

Source: BNY Investments. Annual income paid for the fund year 1 July to 30 June by the BNY Mellon Multi Asset Income Fund W Income shaer class from in investment of £100,000 at inception on 4 Febryary 2015. Regular income is paid montly in 12 equal instalments with the balancing payment paid at the end of fund year. * Income is shown is that attribute to the period from inception on 4 February 2015 to 30 June 2015.

2014/15* 2015/16 2016/17 2017/18 2018/19 2019/2020 2020/21 2021/22 2022/23 2023/24

Reframe your thinking

The big picture? A natural approach to income in retirement

“Variability of income complicates retirement planning”

“Income can be structured to pay a set monthly amount – just like a salary – as well as an annual bonus”

Adviser Risha

Provides a regular income stream without selling investments

Aims to maintain capital, supporting income sustainability

Avoids sequence of returns risk

Is intuitive and gives peace of mind

“Stable and predictable income from the fund allows stable income withdrawals from tax wrappers so simplifying admin”

“Natural income is operationally complex and frankly a bit of an administrative nightmare”

Operations manager Mary

“Prioritising income often comes at the expense of capital return”

“You don’t have to choose between income and capital growth”

Analyst Anthony

Overall yield

4.9

Source: BNY Investments. This is a hypothetical example provived for illustravive purpose only.

£ 23,692

£ 100,000

£ 123,692