sponsored by

The ESG investment debate has rumbled on for a long time, but new ideas and challenges to established thinking continue to emerge. We highlight the lessons learnt from seasoned investors in the field and consider the threat posed by those who want an abrupt reversal in course. We also uncover potential areas of growth, ethical dilemmas around AI and what shape company visits could take as the world grows increasingly uneasy about carbon emissions. Chris Sloley, Editor, Citywire Selector

Into uncharted territory

Embracing the ESG transformation

sponsored by ABN AMRO Investment Solutions

Lifting the lid on the anti-ESG campaign

Under attack

Janus Henderson’s Hamish Chamberlayne on a decade of running sustainable funds

Manager profile

Tackling carbon: Why investors need to act

sponsored by AXA Investment Managers

Up in the air

To fly or not to fly? The pros and cons of meeting in person

Watch this space

Fund managers talk investing in surveillance tech

Catching on

How private capital is chasing the carbon capture market

The start-ups that grew old

sponsored by Comgest S.A

Let’s get our portfolios to net-zero by 2050.

sponsored by Pictet Credit Suisse Asset Managment

Hidden corners of sustainability-related innovation

sponsored by Wellington Management

It is far better to drive change from the inside by having open and honest conversations with senior management and the board than to walk away and immediately lose any leverage for change

More articles:

Lorem ipsum dolor sit amet, consectetuer adipiscing elit

5

Staying power

Clean versus dirty energy

The what, where and how of impact investing

Greenflation: a fair cost or an obstacle?

sponsored by Candriam

The challenge for asset managers in the climate crisis

sponsored by Axa Investment Managers

Beyond SFDR: Understanding the ESG credentials of Article 8 and 9 portfolios

sponsored by AllianceBernstein

Selector perspectives on sustainability

Paying attention to human capital

Do gas and nuclear power deserve a sustainable badge?

Red flags on green bond labels

Venture capital roadblocks on ESG

Hamish Chamberlayne, Janus Henderson Investors

‘If you’re thinking about growing wealth over the long term, it should be perfectly aligned with thinking about big sustainability issues’

Hamish Chamberlayne has been successfully running sustainable funds for more than a decade. The Janus Henderson stalwart talks about bubbles, investment discipline and why he’s never liked the ESG acronym ESG has evolved hugely in a relatively short space of time. Hamish Chamberlayne, who has covered this area for more than 10 years at Janus Henderson, believes there is more to making returns in this space than many might understand. Having started work on the Janus Henderson Global Sustainable Equity fund 11 years ago, Chamberlayne said ethical investing has changed a lot in a relatively short space of time. ‘Looking back to 2011, when I first started working on the sustainable equity strategies, it was a very small and niche market. We only had a fund that was being sold in the UK market and were very narrowly focused in our distribution,’ he said. ‘There wasn’t a huge competitive market in terms of sustainable investment strategies and there was still a lot of emphasis then on exclusionary screening. ‘Predominantly, our investor base was comprised of ethical clients with ethical considerations. That was pretty consistent over really the first 15 to 20 years going back to 1991, when the fund started. In the 90s and the early 2000s, it was definitely that market that you were looking at.’ Chamberlayne said their funds have always had ‘quite comprehensive screening criteria’. ‘We've always been a low-carbon strategy, had high environmental standards, no chemicals of concern, no intensive farming and no contentious industries. We look for businesses that have got very clean profiles.’ He said ethical investing has really become mainstream in the last decade. ‘Over the last 10 to 12 years, you’ve seen the rise in interest in sustainable investing and that’s coincided with the realisation that a lot of big investment trends have emerged that are aligned with sustainable development. ‘We’ve gone from a position where I remember giving presentations back in 2013 and 2014, saying we expect in 10 years’ time that renewable energy will be cheaper than gas and coal. I can now stand here today and say that’s a fact.’

Ian Heath Senior Reporter, Citywire Selector

ESG doubts A staunch proponent of sustainable investing, Chamberlayne said Janus Henderson was nevertheless wary over the use of the ESG label. ‘We’ve always been very careful not to call ourselves ESG investors. I’ve never liked the acronym ESG. It’s become used in many different ways and it means different things to different people,’ he said. ‘I’ve always felt that from an understanding or intellectual perspective, it doesn’t make sense to put the E, S and G together. It’s such a huge spectrum of different topics and collapsing it all into the single acronym I’ve always felt was a risky way to characterise the industry. ‘People need to look at the underlying investment strategy. What we have always focused on is saying: “This is our strategy and we’re aligning our view to areas which we think are aligned with sustainability and growth.”’ He said that this caution led him to avoid investing in what he described as the ‘ESG bubble’. ‘Last year, we were very worried about bubble-like characteristics in the markets – meme stocks and a lot of things attached to ESG. We talked about the ESG bubble and we didn’t invest in any of the ESG-related IPOs because we see them as just being story stocks.’ Don’t forget the fundamentals During the last three years, Chamberlayne has generated average returns of 35.5% on the sustainably-focused funds he manages and had a Citywire AAA rating for the whole of 2021. He said that maintaining ‘fundamental discipline’ in stock picking was a key aspect of this success. ‘We’ve kept a very strong investment discipline in our fundamental analysis, and we want to see purity in terms of our alignment with sustainable companies. We do have high standards around our thematic classifications and exclusionary criteria but we also have high standards on our fundamental research. ‘When you look at the financial profile of the companies that we invest in and our portfolio construction, we are focused on companies that have growing revenues, attractive business models, good margins, good cashflows and good returns on invested capital. ‘We are looking for growth but when we hit more volatile economic times, we want to have companies with solid fundamentals that can see us through.’ A sector he identified as key to the sustainability agenda was the tech industry.

‘We are getting into the territory of the fourth industrial revolution – the green industrial revolution, where you’re getting this merging of our technological and industrial economies, and the power of technology is being unleashed on many different industries. ‘In the automotive sector, cars have gone from being basically mechanical to much more like computers. You can apply this to the aerospace industry, the mining industry, real estate, infrastructure, finance or healthcare. ‘Autodesk, the world’s leading design software company, has a very exciting future ahead of it still. It is used by 60% of the world’s architects and engineers. Sustainability starts with design and their software helps architects and engineers design more sustainable buildings and more resilient infrastructure.’ Stay aligned Chamberlayne said the key word for him when it came to sustainable investment was ‘alignment’. ‘That’s the North Star when it comes to sustainable investing. If you’re thinking about growing wealth over the long term, it should be perfectly aligned with thinking about big sustainability issues,’ he said. ‘The best companies are thinking about these big trends that are shaping the global economy – the environmental and social trends. Companies that are navigating those trends and strategically managing their operations, with a view to all the potential risks to their business, are the businesses that are most likely going to generate long-term wealth.’

This might be the opportunity to reset and make the kind of intuitional changes and policy choices that will lead to a better, greener and more sustainable future

Audrey Ryan Support manager, Aegon Global Sustainable Equity Fund

Aegon Global Sustainability Equity Fund

Consolidation of ESG metrics in investing has become standard practice. One company takes a unique approach. As investors pay more and more heed to where their money is placed, ESG investing harvests wide momentum. No longer the niche product it once was, it is now the heart of the asset management industry – and companies are finding innovative new ways to remain ahead of a changing industry. With ESG commitment at the heart of its business model, ABN AMRO Investment Solutions (AAIS) offers a suite of ESG and sustainable strategies. Most of them are managed by what they describe as ESG Originals, which are typically investment boutiques that were founded to be responsible investment shops. Jaouad Olqma, senior analyst European equities at AAIS, said: ‘As an example, EdenTree, available on our sub-advisory manager platform, has been including positive ESG screening since 1988, giving them a process fully integrated and a strong knowledge of the universe. The long-term track record of the strategy reflects the process as it is now, with no change through the time, giving us transparency in our analysis.’ Eric Gerritse, senior analyst US equities at AAIS, said: ‘About five to six years ago, ABN AMRO Investment Solutions decided it wanted to add a suite of genuine ESG and sustainable strategies to its Luxembourg-based existing sub-advisory manager platform. We started looking for managers or asset management firms that had ESG or sustainable criteria in their decision-making process. This was the starting point for us. ‘Such companies have dual objectives, generating financial returns and ESG performance. Proprietary ESG research and engagement are in their DNA and this has been the case right from day one when these firms were founded.’ He added: ‘There are about seven of such companies in the US – what we describe as ESG Originals. For example, Boston Trust Walden, Boston Common or Parnassus – which are on our platform – are all ESG Originals.’ Olqma added: ‘ESG Originals are active in participating to the transition to a sustainable world. We identify their leadership and build a relationship with them on the long term. Selecting them supposes to invest time, higher than when selecting mature companies, but we have the people in ABN AMRO Investment Solutions to go on-site, take the time to understand the DNA of the boutique and secure the full process from the operation due diligence step to the selection of the manager.’ Doing the homework Gerritse emphasised that the managers they select need to perform their own ESG research in order to generate unique insights and differentiated views. This is vital given there are a limited number of third-party data agencies whose ratings are relied on not only by many active managers but also by passive ETF indices alike. Given this demand, a funnel is created that pushes oodles of money into the same companies. This, with the fact that third party rating companies tend to have backward-looking perspectives, makes it vitally important to conduct in-depth proprietary and forward-looking ESG research – something that Boston Common, Boston Trust Walden, Parnassus and EdenTree all do. This leads to the next strategy used by ABN AMRO Investment Solutions: ESG momentum. Gerritse said: ‘If you’re able to invest in stocks of companies that are experiencing a positive ESG dynamic before the market acknowledges this positive change, then you have more opportunities to generate alpha. ‘Boston Common, which is the sub advisor for our ABN AMRO Boston Common US Sustainable Equities Fund, for example, is not dogmatic about any one particular alpha source. They have a value style and invest in ESG leaders, ESG momentum opportunities and Solution providers to the world’s challenges but the breakdown of the portfolio over these alpha sources also depends on the attractiveness of stocks from a valuation point of view. ‘Engagement by Boston Common is another key differentiator. ESG momentum and engagement go hand-in-hand: identifying a good, undiscovered ESG momentum opportunity can be facilitated by an engagement approach. The latter might speed up the valuation opportunity as companies get re-rated.’ Good governance has been a key issue. The strategy’s success relies on a strong partnership and the ABN AMRO Investment Solutions team believes external managers are the ones that make the difference in the sustainable universe. Olqma said: ‘Building trust and sharing knowledge are very important aspects of long-term partnership. By sharing knowledge with our delegates, we are analysing a topic from different angles. This diversity is key when adapting to changes such as the SFDR regulation, where you need to interpret elements that are never black or white. Waiting for the harvest Over a period of time, ESG has become the standard for businesses across industries. Getting the ESG proposition right creates a path to high-value creation. ‘You can invest in ESG leaders but you have to identify the leaders before they become leaders because then you have an alpha source’, said Gerritse. ‘The value investing style is probably benefitting most from an ESG momentum and engagement approach. The intrinsic value of a stock is determined by discounting future cash flows using a discount rate, which includes ESG risks as part of the risk premium. ‘Stocks can be undervalued as the actual ESG risk might be lower than the perceived ESG risk profile. This relates well to an ESG momentum strategy that is backed by an engagement effort.’ ABN AMRO Boston Common US Sustainable Equities, ABN AMRO Walden US Sustainable Equities and ABN AMRO EdenTree European Sustainable Equities are unique propositions, being ESG and value-strategies. Boston Common is a sustainable strategy that tries to exploit inefficiencies in the market based on misvalued ESG momentum and ESG leaders. All the stocks in the portfolio provide solutions to Boston Common’s three ESG focus areas. Boston Trust Walden is a high-quality value ESG strategy but it has a more defensive return profile. ‘By integrating ESG criteria, you have a different shape of portfolio also. Usually, when you look to the value space, undervalued stocks goes with a cyclical bias in your portfolio, meaning valuations can be unlocked by the improvement of the economic cycle. When you build ESG value strategies as EdenTree is doing, valuations can also be unlocked by a strong ESG integration and engagement. It leads to a more diversified portfolio,’ added Olqma. No doubt about it, ESG is here to stay. And companies are finding innovative new ways to tap into that prospective fountain. ‘For a long time, investors have considered the integration of the ESG as a reduction of the universe, so lower potential source of alpha,’ Olqma said. ‘The truth is that we are in a world where both are closely linked. It is about identifying the ESG risk, but also finding new opportunities in proposing solutions to the transition. EdenTree has been integrating those aspects, providing a strong risk adjusted performance on a five-year period.’ Reach out if you wish to learn more: aais.contact@fr.abnamro.com Further information on the sustainability of the funds is available on www.abnamroinvestmentsolutions.com. Investment decisions should be based on a review of all fund documentation including the KIID and the prospectus taking into account the investment policy objectives of the fund. Final investment decisions should not be made on the basis of this communication alone. For more information about the risks and the fees of the fund please refer to the KIID and prospectus. The opinion expressed above is as of the date of this publication and is subject to change.

Jaouad Olqma Senior Analyst European Equities at ABN AMRO Investment Solutions

By:

Sponsored content by

Eric Gerritse Senior Analyst US Equities at ABN AMRO Investment Solutions

Promotional document intended for professional investors.

The ethical investor

The moderate investor

The active investor

The innovative investor

If your client wants their investment portfolio to reflect their strongly held values and beliefs, consider ethical or values-based investing. Some of these funds were originally faith-based and have their roots in religious movements. Others are broader. They will typically use negative screening to remove companies in industries that might be viewed as objectionable from an ethical or moral perspective. They might screen out companies associated with alcohol, tobacco, gambling, pornography, animal testing, weapons and nuclear power, for example. This type of investing is typically quite personalised, as everyone’s moral compass is calibrated differently. What is acceptable to one investor might not be to another.

If your client requires their investments to stick closely to traditional benchmarks but they are happy to screen out the most unsustainable companies, consider an ‘ESG lite’ approach. By investing in the world’s largest companies, there will be some compromises on ESG issues. These companies will not score highly on every factor, although there is a great deal changing, especially since the pandemic. A moderate approach uses negative screening to avoid companies with the lowest ESG scores. This strategy lends itself to investing in less expensive ESG-themed ETFs and index trackers.

If your client wants to choose companies that rank as the most sustainable according to ESG metrics, as opposed to excluding the ones that rank lowest, positive screening could be the best approach. ESG strategies using positive screening seek out companies that are the best in class and score highly on a range of different ESG metrics, including environmental impact, treatment of workers and business ethics. They also use negative screening to exclude companies with the lowest ESG scoring from their investment universe.

If your client wants their investments to support companies creating solutions to world problems, impact investing could be the strategy to follow. The aim of impact investing is to make a positive and measurable impact on society or the environment, as well as generating a financial return. Some impact investing focuses on funding specific projects, such as microfinance funds to create affordable housing, or green bonds to raise money for a clean water initiative. This may mean the portfolio is more concentrated, and there is a good chance it is riskier too. Investors in this space need to be willing to accept more risk and less diversification.

Anti-ESG: the rise of ‘InfoWars investors’

Vivek Ramaswamy, Strive Asset Management

Alyssa Stankiewicz, Morningstar

‘What the ESG movement has allowed is for governments to get done through the back door what they could not get done through the front door’

Witold Henisz, Wharton School

‘You could go to any major asset manager and ask for an oil fund and pay maybe a third of the fees that Strive is charging you. I don’t see any criticism of that in the press’

Anti-ESG afforded ‘too much credibility’ For Harms, who has spent more than 15 years in financial marketing, Ramaswamy’s Fox News appearances and Strive Asset Management’s fund marketing – both directed to regular mom-and-pop investors – are mischaracterising ESG in a way that shows bad faith. ‘That’s a moral issue for me. These people are being sold a conspiracy,’ said Harms. ‘It reminded me of what Trump did with Stop the Steal, where he raised hundreds of millions of dollars. Using conspiracies works, and I think Vivek understands that. You can tell by the way he shows up on all the right channels.’ In writing an op-ed comparing Ramaswamy to far-right radio show host Alex Jones, and Strive Asset Management to InfoWars, Harms hoped to highlight the connection between the anti-ESG movement and wider Republican disinformation efforts. He’s not the only one. The left-leaning non-profit and media watchdog group Media Matters for America recently issued a similar warning. Witold Henisz, vice dean and faculty director of the Wharton School’s ESG Initiative, is also concerned.

When Henisz first noticed the anti-ESG movement, he felt like he’d seen it before. He used to study the fake news cycle as part of his research into political and social risk management. Now, it had suddenly entered the financial industry but Henisz felt it wasn’t being called out as such. ‘I think the anti-ESG movement is being afforded way too much credibility,’ Henisz told Citywire Selector. ‘The media enjoys battles, and two titans pitted against each other is compelling. But this isn’t one of those stories. Instead, ESG is being attacked in a way that’s creating a false narrative of there being a legitimate challenger. ‘I don’t see enough interrogation of why this is happening now, who’s funding it, and how well it’s actually going,’ he added. The facts behind the phenomenon There’s a lot of noise coming from the anti-ESG movement, but there are few products catering to the cause. Alyssa Stankiewicz, associate director of sustainability research at Morningstar, said there are currently no funds in Europe that could be called anti-ESG, and only four such products in the US.

Two of these are from Strive Asset Management: the Strive US Energy ETF (DRLL) and the Strive 500 ETF. Then there’s the Bad ETF, launched in December 2021 by The Bad Investment Company, to track US gambling, alcohol, cannabis and pharmaceutical large-cap stocks. And let’s not forget Constrained Capital’s ESG Orphans ETF, launched in May 2022 to track industries commonly excluded by sustainable funds. The largest anti-ESG fund to date is Strive’s US Energy ETF, which caused international headlines when it attracted more than $300m in the three weeks after its launch. Henisz believes the announcement should have been met with more scepticism. ‘You could go to any major asset manager and ask for an oil fund and pay maybe a third of the fees that Strive is charging you. I don’t see any criticism of that in the press. I only see articles about how DRLL has raised $315m so quickly, and how incredible that is,’ he said. ‘I wouldn’t be surprised if some of the same high-net-worth individuals funding the Republican attorney generals are also investing in DRLL to create some initial buzz,’ he added. A look at the anti-ESG fund with the longest record of monthly fund-level net flows available on Morningstar, shows the initial hype proved short-lived. The Bad ETF attracted $8.3m in inflows when it launched in December 2021, but these dropped to $686m in January 2022. The following month, it lost $282.5m in outflows. As of 21 September, it has $7.78m in assets – less than it amassed in its first month of launching and considerably less than $515.37m, the average fund size in Morningstar Direct’s list of sustainable US funds.

A number of commentators say the anti-ESG movement is a disinformation campaign with ties to the ‘Great Reset’ conspiracy theory, and they are worried it isn’t being treated as such It’s a Thursday night in February 2022, and Fox News host Tucker Carlson has just asked Vivek Ramaswamy, CEO of Strive Asset Management and author of Woke, Inc., to sum up ‘Larry Fink and his agenda’ for the show’s viewers. Ramaswamy explains that BlackRock ‘causes companies to bend their knees to woke orthodoxy’, and that $10tn belonging to everyday Americans is being weaponised in ways that would make their blood boil. ‘But Tucker, there’s one more part that makes this story even take a darker turn,’ Ramaswamy says. Click here for article ‘The puppet master behind the scenes of BlackRock is, of course, China. ‘We’re going through this thing that everyone calls the Great Reset, the stakeholder capitalism revolution, where we dissolve the boundaries between government actors and private companies to advance a single progressive globalist agenda,’ he adds. This is one of several times that Ramaswamy has argued that ESG is part of the ‘Great Reset’, a conspiracy theory claiming that a global elite is using the Covid-19 pandemic to establish a new world order. Ramaswamy doubled down on this idea in July, when he spoke on rightwing activist Charlie Kirk’s podcast, using the US Green New Deal as an example: ‘What’s really happening here, Charlie, is that you have lurking state action behind the scenes. What the ESG movement has allowed is for governments to get done through the back door what they could not get done through the front door.’ The conspiratorial rhetoric is a far cry from the several opinion pieces Ramaswamy will go on to write for The Wall Street Journal, or the nuanced interviews he will give to Financial Times and Bloomberg, during the same period. This, according to Ryon Harms, CEO of ethical marketing agency Manifest Social, illustrates that there are two Vivek Ramaswamys – each catering to a different audience. ‘When you read Ramaswamy’s op-eds you think “Okay, maybe I don’t agree that oil is a great investment, but it’s a perspective, and you have to respect that in a free market”,’ Harms said. ‘But when I started following him on Twitter, I realised that everything he does is wrapped in conspiratorial language – how they, the global elite, want to control our lives, how they want to destroy the economy. That’s the general theme whenever he talks about ESG,’ he added.

Siri Christiansen Reporter, Citywire Selector

A similar news buzz was attempted during this year’s proxy voting season, where 43 anti-ESG shareholder resolutions were filed by two known conservative shareholders and one undisclosed shareholder. But these resolutions, Henisz said, were not designed to shape corporate policy or to actually win, but solely to generate headlines. Many of the proposals asked companies to explore the impact of diversity, equity and inclusion practices on their white employees, and others addressed legitimate governance or disclosure issues similar to those from pro-ESG groups. ‘I don’t think there’s enough criticism about whether the anti-ESG proposals even make sense. One of them asked Disney to divulge human rights issues in their supply chain – but that’s more like an ESG proposal. Don’t give them that,’ said Henisz. A Morningstar analysis of the support for anti-ESG proposals further demonstrates the anti-ESG movement’s lack of wider industry support – the proposals received only 7% of support on average, compared with the 30% average support for resolutions by other shareholders. The cost of anti-ESG As of September 2022, at least five states – West Virginia, Idaho, Oklahoma, Texas and Florida – have created new policies and laws restricting business with asset managers that include ESG factors in their investment process. But the high costs incurred through having to deal with smaller fund houses, which typically charge higher fees, together with a lack of evidence regarding the long-term financial benefits of an anti-ESG stance, mean that few states are likely to follow in their footsteps, said Henisz. ‘They talk about managers needing to observe their fiduciary duties – well, the Texas comptroller should be observing his fiduciary duty to the Texas taxpayers, and that includes not spending over $500m more than he needs to on municipal bond issuance. So I don’t see this taking over or becoming this huge wave. But it is a threat,’ said Henisz. He added that while Ramaswamy and the Republican governors are claiming that radical leftists have captured the investment industry, the truth is that Fink is ‘the epitome of conservative financial management’. ‘The fact that they’re as conservative as they are and still making progress on ESG only highlights how obvious it is as a good future investment. ‘But the ESG opposition is not drawing from investment expertise, it’s drawing from people from political backgrounds who are more focused on the upcoming elections than on long-term financial performance,’ Henisz said. Strive Asset Management had not responded to Citywire Selector’s request for comment by the time of publication.

2021 was one of the warmest years on record – and the seventh consecutive year when the global temperature has been more than 1°C above pre-industrial levels [1]. This is worryingly close to the cap envisaged by the 2015 Paris Agreement, to limit global warming to +2°C (but ideally +1.5°C) above pre-industrial levels [2]. All the evidence suggests the reason we have edged ever closer to that proposed limit is the high and growing levels of carbon dioxide in the earth’s atmosphere. The carbon challenge We need to bolster and accelerate our efforts to tackle climate change – carbon emissions need to be reduced by 45% by 2030 and reach net zero by 2050. This means dramatically cutting our greenhouse gases (GHGs) and moving the global energy sector away from fossil-based fuels, towards greener, renewable alternatives. If we don’t, we may jeopardise the global economy and the prospect of a prosperous future. Thankfully, many governments and organisations are stepping up to the challenge. More than one third of the world’s 2,000 largest public companies have net zero commitments, up from one fifth in 2020 while 91% of global GDP is now captured by national government net zero targets, up 68% over the same period [3]. Industries such as automobile makers are transforming with Ford and Jaguar Land Rover having committed to having all-electric ranges in the next decade [4], while oil giants BP and Shell have set their own net zero targets [5] [6]. Why investors need to care Investors need to be aware of the risks of investing in businesses that will underperform because of their environmental footprint. In our view, delivering climate-aware investments is not something that challenges the primacy of financial objectives – it complements and enhances our understanding of those objectives. Fundamentally, it’s about better management of financial risk. Thankfully, it is increasingly possible to use analysis, data, and portfolio construction techniques to align portfolios with the ambition of a net zero carbon world. When it comes to selecting securities, it is vital to assess how climate change could impact a particular business and its future profitability. How would a firm be impacted by flooding and other disruptive weather events? What would it mean for its operations, supply chains and workforce? There are regulatory and fiscal risks too. Governments can increase taxation to address the impact of emissions. If companies are going to have to pay more to emit GHGs, then that will hit their profitability and, subsequently, investor returns. Consumers can vote with their feet too. They can reduce demand for a company’s goods and services if it is seen to be at risk from climate change or if it is contributing to rising emissions. New opportunities But it’s not just all about risks and exclusions – there is the opportunity to invest directly in green assets: green bonds, green real estate, forestry and so on. Equally, the new technology being employed to help the transition to a cleaner economy may provide a series of opportunities for investors. This technology, that is both directly and indirectly related to the energy transition, is evolving rapidly. We are already seeing fairly mature developments in solar and wind and other renewable energy sources, but they still must scale up massively to contribute fully to the fight against climate change. Technology directed towards improved energy efficiency also provides investment opportunities and growth potential. At its heart this is about investors understanding and adapting to the risks that climate change poses for business models and to communities. Companies with poor environmental footprints and poorly thought-out carbon pathways may underperform, while at the extreme end we may well see stranded assets rendered un-investable by the pace of policy or consumer change. It is widely agreed that climate change poses a huge threat to the world. We know that it is going to be very damaging to the environment. It will result in rising sea levels, extreme weather, societal disruption, the loss of economic activity and more. Quite simply, without the transition to a low carbon economy, we won’t have sustainable economic growth, and that would mean we can’t have sustainable investment returns.

Chris Iggo AXA IM, CIO Core Investments

Disclaimer This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision. Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries. © 2022 AXA Investment Managers. All rights reserved

[1] 2021 joins top 7 warmest years on record: WMO | | UN News [2] The Paris Agreement | United Nations [3] Net Zero Stocktake 2022 | Net Zero Tracker [4] Ford and Jaguar Land Rover commit to only electric cars by 2030, Production Engineering Solutions, 2021 [5] Shell unveils plans to become net-zero carbon company by 2050, The Guardian, 2020 [6] Companies referenced here are for illustrative purposes only and do not constitute a recommendation for an investment strategy or a personalised recommendation to buy or sell securities

Please click here for more information on AXA Investment Managers approach to responsible investing.

• If we don’t transition to a low carbon economy, we won’t have sustainable economic growth • Investors need to be aware of the risks of investing in businesses which will underperform because of their environmental footprint • There are growing opportunities to invest in green assets and new technologies helping drive the transition

Private capital is chasing carbon capture deals but questions remain over the technology’s efficacy. We talk to investors and experts in the field about the opportunities and challenges Private equity and venture capital investors have been pumping millions into carbon removal or capture technologies, but critics say these businesses only enable companies to continue polluting. PitchBook analysts estimate the overall market for carbon and emissions tech will reach $905bn by the end of the year and $1,377bn in 2027. In carbon capture specifically, in 2017, there were only three deals worth $16.6m in carbon capture startups, according to PitchBook. So far this year, investors have poured around $1bn into 19 investments in the sector, almost triple the amount spent in 2021. There are two different technologies: point-source carbon capture and storage, which sequesters CO2 at source; and direct air capture, which removes CO2 from the atmosphere. Some of the biggest deals in the last few years have included a CHF600m (€627m) raise by Climeworks and a $150m raise by Carbon Clean – both completed this year. Businesses aiming to tackle the issue of carbon capture are not new. But recent interest in the sector from private equity and venture capital investors has partly been driven by a change in the cost of carbon in the EU, according to Fabio Ranghino partner and head of strategy and sustainability at Ambienta.

As the price of carbon increases it will trigger more investment in clean technologies to reduce emissions, particularly in high-emitting industries. Because companies currently need to buy permits when they pollute. Further reforms to the EU carbon market are expected to increase demand for CO2 permits and drive up the price. The other change has been the acknowledgement in the UN Intergovernmental Panel on Climate Change’s (IPCC) latest report of the need for carbon capture. It estimated we need to remove up to 1,000 gigatons of CO2 from the atmosphere by the end of the century. Currently about 40 megatonnes of CO2 are captured and stored annually. Carbon capture under fire However, the IPCC report has also come under criticism. Lindley Mease, director of the Clima fund, said in a commentary written on conservation news portal Mongabay, that the recent recommendations have been influenced by fossil fuel stakeholders.

‘Can Climeworks as an organisation scale in a global fashion to make sure we have the associated value chain, site selection, and infrastructure for transport and sequestration, to deliver a whole solution?’

Esther Peiner, Partners Group

She said a senior staff member of Saudi Aramco was a lead coordinating author of the report, while a staff member at Chevron reviewed the chapter on energy systems. She noted: ‘In light of this endorsement, it is important to note that most carbon capture technologies are unproven, dangerous, or financially impractical. Moreover, these approaches would enable the perpetuation of the fossil fuel industry by using their infrastructure and softening the pressure on the phaseout of fossil fuels that was needed, like, yesterday.’ Climate activists Citywire has spoken to have also said carbon capture is nowhere near the scale needed to make a difference. For example, Kim Bryan, associate director of communications at 350.org, a climate movement website, said the world should stop burning fossil fuels and reduce emissions, instead of relying on some future technology. Fossil fuel companies have been criticised for using carbon capture as a way to greenwash. Research by Tyndall Centre last year found that 81% of carbon captured to date has been used to extract more oil. Ambienta’s Ranghino agrees that some of the focus on carbon capture is allowing emitters to continue business as usual and rely on fossil fuels. ‘As an asset manager, money tends to flow where there is an economic case, so it’s the duty of the regulator to make sure the money is funnelled in the most effective way to reduce emissions,’ he said.

Selin Bucak Alternatives Correspondent

The need for scale His colleague, Saverio Zefelippo, an associate in the sustainability & strategy team, added that scalability is an issue. He said: ‘Up to today most projects out there pump CO2 that is captured underground to facilitate the production of oil. They are not contributing to solving the problem. Another big way that carbon removal and credit are generated today is preventing forests from being cut down. ‘There are questions around the actual effectiveness of these projects. The truth is we need both reductions and removals. So, all companies should act on both ends, but there should be a regulator that is guiding these efforts.’ Switzerland-based Partners Group has been an investor in carbon capture technologies, most recently participating in the funding round for Climeworks. For Esther Peiner, the firm’s managing director and co-head of private infrastructure in Europe, the transition away from fossil fuels is going to be slower than anticipated, which increases the need to address historic concentrations of emissions. Current technology can be expensive, but she believes ‘the world will need to pay the bill for its emissions’ and that the ‘higher cost of direct air capture and sequestering is the only way we will be able to meet our net-zero goals’. In her opinion, the technology will scale over time and the cost will come down. But one concern is the speed and technology of scale-up. ‘Supply chains will need to evolve to help multiply the size of the projects. The other point is, as the supply chain scales, can Climeworks as an organisation scale in a global fashion to make sure we have the associated value chain, site selection, and infrastructure for transport and sequestration, to deliver a whole solution?’ she said.

HOME OF THE WORLD'S OLDEST COMPANIES Japan is the home of the world’s oldest companies and boasts one of the highest concentrations of large family-run businesses on the planet. At the start of the 21st century, one third of all Japanese listed companies had some kind of family control [1] and that remains the case today. Japan’s tendency to corporate family ownership can be explained by its relatively recent industrialisation. First, an industrial and service infrastructure of family companies sprang up alongside and became symbiotic with the state-affiliated enterprises which pushed the country into economic modernity. Second, Japan’s economic miracle of the 1970s is so recent that many founders from that era are still in charge. We believe investors should pay close attention to these businesses, perhaps more than they do at present. We have observed many cases globally when family or founder-owned or run companies align well with shareholders’ interests, and in Comgest’s Japan portfolio we take that idea quite far. About one third of our holdings is from companies which fit that definition. Some examples are Fast Retailing, Nidec, Keyence, Softbank, Pan Pacific, Nihon M&A, Hoya, Obic, Sushiro, Peptidream, and Kobe Bussan. Simply put, we view these companies as having a ‘Day Zero’ mentality which translates naturally to capital discipline with a long-term mindset, through the pursuit of unique businesses. These are start-ups which grew old. They speak the language of the shareholders because they are run by a major shareholder. With not just skin, but blood sweat and tears in the game, they certainly seek returns but importantly, they also seek long-term survival. They are the original ‘ESG’ plays before ESG existed; they fulfil a sustainable social role and their capital allocation choices have rewarded our trust.

IMPORTANT INFORMATION Data as of 31 August 2022, unless stated otherwise. This marketing communication has been prepared for professional/qualified investors only and may only be used by these investors. Investing involves risk including possible loss of principal. All opinions and estimates are current opinions only and are subject to change. This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The views expressed in this document are valid at the time of publication only, do not constitute independent investment research and should not be interpreted as investment advice. The Japan portfolio mentioned herein refers to Comgest Growth Japan, a UCITS compliant sub-fund of Comgest Growth plc, an open-ended umbrella-type investment company with variable capital and segregated liability between sub-funds incorporated in Ireland and authorised by the Central Bank of Ireland and managed by Comgest Asset Management International Ltd. Before making any investment decision, investors must read the latest prospectus and Key Investor Information Document (“KIID”). The Prospectus, the KIID, the latest annual and interim reports and any country specific addendums can be obtained free of charge at our offices or on our website comgest.com. Comgest S.A. is a portfolio management company regulated by the Autorité des Marchés Financiers (AMF) whose registered office is at 17, square Edouard VII, 75009 Paris, France. Comgest Asset Management International Limited is an investment firm regulated by the Central Bank of Ireland and registered as an Investment Adviser with the U.S. Securities Exchange Commission. Its registered office is at 46 St. Stephen's Green, Dublin 2, Ireland.

Richard Kaye Co-manager of the Comgest Growth Japan fund

[1] From 1962-2000: source Financial Times, "How Japan’s family businesses use sons-in-law to bring in new blood", (https://on.ft.com/2Xrvftc).

Richard Kaye Analyst / Portfolio Manager, Japanese Equities

‘A ‘Day Zero’ mentality translates naturally to capital discipline with a long-term mindset, through the pursuit of unique businesses’

OBIC Obic is one of Japan’s leading business software providers and the country’s answer to Oracle for small companies. Since its creation in 1968 by Masahiro Noda, (who remains Chairman and 24% shareholder) it has insisted on keeping all operations home-grown: no sales agents, no mid- career hires. ‘We are like the Chairman’s children’, say Obic staff. That may sound odd in the West, but it has created a consistent and reliable service provider in corporate Japan which is heading Japan’s software solutions to address its labour shortage. NIHON M&A CENTER Similarly to Obic, Nihon M&A Center is an indispensable presence among small Japanese companies but as a succession advisory firm, is suffused with the founder culture of 10.4% holders Mssrs. Miyake and Wakebayashi. Nihon differs from Obic in its openness to outside talent but shares with Hikari Tsushin that ruthless focus on capital return, efficiency of process and gross profit per employee, traits one would associate with a shareholder-managed company. Just recently we spoke with Mr Miyake, and he explained how he regularly sells stock to colleagues to bind them more directly into the destiny of the company. PERMANENT START-UPS These firms are not the sleepy, hidebound companies one might unkindly expect based on their ownership structure. Rather, as Japan’s domestic investor base returns to its local market by increasing their allocation to Japanese equities after two decades’ hibernation, these efficient capital allocators, these permanent start-ups, are a part of the investible universe which is naturally winning attention. Comgest is pitching its tent there, too. Read our Investment Letters here

HOYA Hoya Corporation, which has parried its core strength in glass processing into near dominance in disc substrates and semiconductor imaging materials, is a classic case. This family glassware business gained national renown from supplying US occupation authority buildings. The company’s willingness to divest its legacy crystal ware business and the camera business, to which many Japanese companies are unprofitably wedded, or to build a contact lens retail network in Japan which draws on Hoya’s ophthalmic presence but sells other companies’ lenses because that is more profitable, all reflect this flexibility and almost ruthless pursuit of return. When we asked founding family member and (former) Chairman and President Hiroshi Suzuki, which businesses he kept and why, his answer was as if from a textbook: ‘the company is not mine; any business can grow old and we constantly need to consider divesting’. The words are not from a book, though; they express how he really felt at the interstices of his organisation. Hoya’s idiosyncrasy in pursuing return and in transparency manifests itself also in the fact that another family member regularly opposes the management at AGMs. As Mr. Suzuki has hinted wryly, a Hegelian dialectical approach to discussion has led to great decisions, but long and difficult meetings.

Hiroshi Suzuki, founder family and former Chairman/President/CEO, Hoya Corp

‘The company is not mine. Any business can grow old and we constantly need to consider divesting’

Japan's family firms not to be underestimated

Stephanie Hare, researcher and author

‘Any country that wishes to remain remotely relevant has to stop being naive on the importance of getting ahead in the AI sector, and act in concert’

Johan Van der Biest, Candriam

‘Investors should be looking at large IT and software companies that are helping their customers in setting up algorithms while helping them to interpret the outcome and implement the conclusions’

‘The US is investing heavily in AI and some of their largest IT companies have been extremely successful in developing AI-based applications. According to Investment Monitor, the US is still ahead of China, but according to RS Components, China is overpowering the US massively in terms of the number of AI application patents,’ he told Citywire Selector. The obvious conclusion from this is that Europe has a lot of catching up to do, he added. Those looking to invest in AI have three main options, said Van der Biest. ‘Investors should be looking at large IT and software companies that are helping their customers in setting up algorithms while helping them to interpret the outcome and implement the conclusions. Second to that, underlying hardware suppliers, such as the GPU [graphics processing unit] or FPGA [field-programmable gate array] manufacturers. And lastly, companies that have embraced AI and machine learning, as these will be able to improve their margins significantly.’

Looking towards China, AI could create €600bn in economic value annually in the country, according to a 2022 McKinsey report, which pointed to the potential of China’s auto market sector, among others. ‘China’s auto market stands as the largest in the world, with the number of vehicles in use surpassing that of the US. The sheer size, which we estimate will grow to more than 300 million passenger vehicles on the road in China by 2030, provides a fertile landscape of AI opportunities,’ the report said. Focusing on the global market more broadly, Van der Biest added: ‘Every single sector is and will be using AI. Algorithms will increase efficiency in every imaginable process, going from reducing energy consumption in the data centre to revealing the structure of the protein universe.’ The ethical input With advancements in AI moving so quickly, it’s key for thematic asset managers to play their part in steering funds more thoughtfully towards the industry. A number of fund managers are already doing this through specific alliances.

Karen Kharmandarian and Alexandre Zilliox, co-managers of the Natixis Thematics AI and Robotics fund both believe in the importance of assessing AI companies’ biases and ethics. As a result, they are part of the Digital Inclusion Benchmark set up by the World Benchmarking Alliance. This initiative promotes ethical AI use and brings investors and companies together to discuss the development and application of AI. ‘We believe that an algorithm will be as good as the people who developed it, which means companies must be extra-careful not to have biased or poor-quality data. They also need diverse teams in terms of culture, ethnicity, social background, and gender,’ said the managers.

Surveillance technology, and the AI behind it, is a multi-billion dollar market with long-term growth ahead. We talk to fund managers about its qualified attractions The AI sector is shaping up as something of a quandary for ethical investors. The potential for human rights abuses around developments such as surveillance technology is obviously unpalatable. However, this is a booming and hugely valuable long-term theme and could surely benefit from investor engagement as well as funds. Stephanie Hare, a researcher and author of Technology Is Not Neutral: A Short Guide to Technology Ethics, told Citywire Selector about the rapid development in this area, particularly among world superpowers, and the ethical issues it throws up as legal frameworks struggle to keep pace. ‘Any country that wishes to remain remotely relevant has to stop being naive on the importance of getting ahead in the AI sector, and act in concert,’ she said. ‘When you see reports about how China’s espionage capabilities could now be on a par with that of the Kremlin, you start to realise how important the issue becomes from a national security standpoint.’ The opportunity It’s clear, then, that global heavyweights will be pouring increasing amounts of money into this space, but how does this translate into identifying specific tech sectors to invest in? Johan Van der Biest, who runs the top-performing Candriam Equities L Robotics and Innovative Technology fund, believes the US and China are still neck and neck in the race to develop AI.

Krystle Higgins Reporter, Citywire Selector

Karen Kharmandarian, Natixis

‘We believe that an algorithm will be as good as the people who developed it, which means companies must be extra-careful not to have biased or poor-quality data’

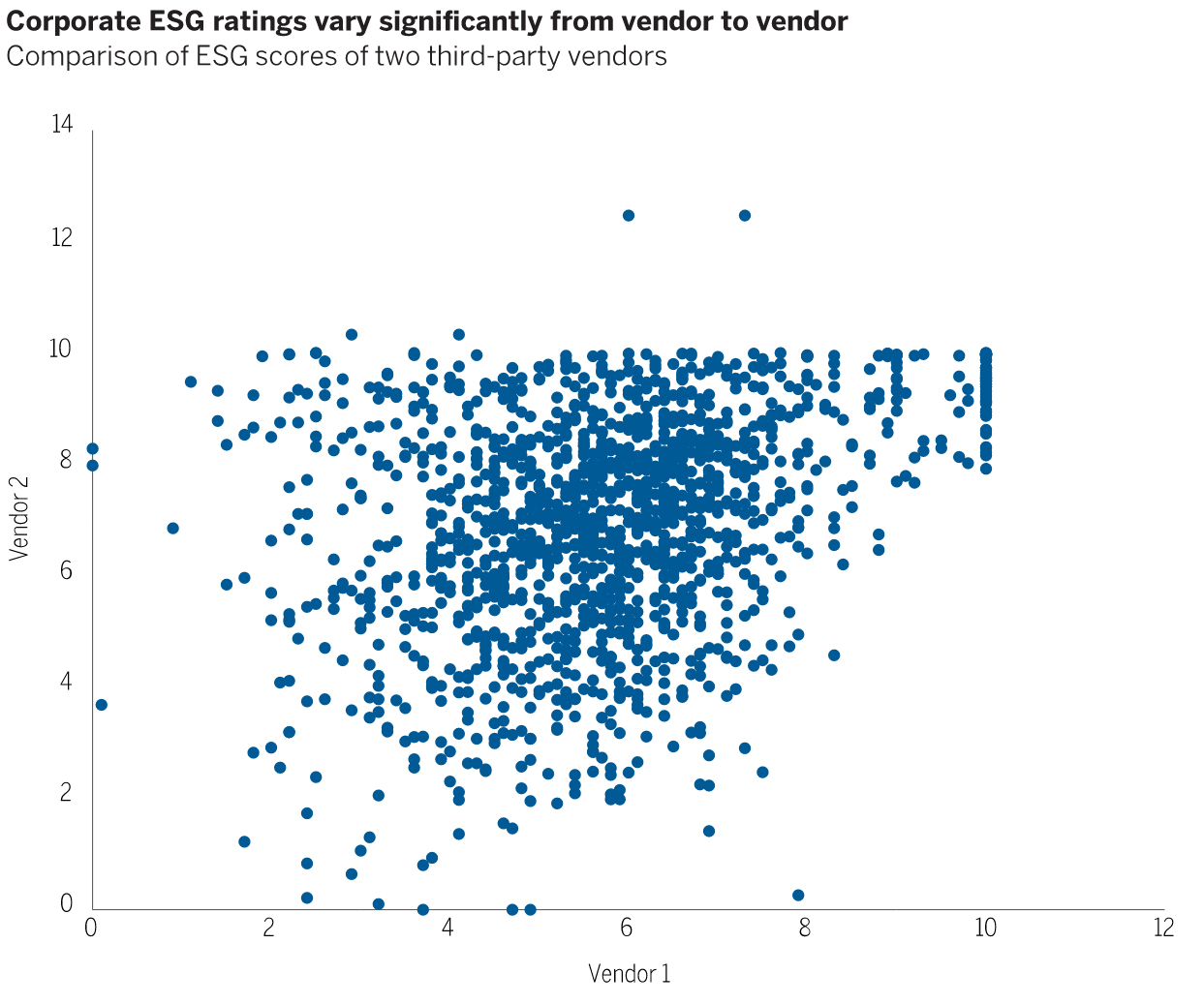

We believe that good ESG practices are a critical driver of companies’ long-term success but identifying these can be hard given the lack of reliable, forward-looking data. This is especially true in the under-researched European small-cap universe. More broadly, we see sustainability as a major driver of innovation and growth. European smaller companies are at the forefront of that innovation as they seek to satisfy a growing customer demand for sustainable solutions. We think this combination of high inefficiency and high opportunity offers active investors significant scope to add value through fundamental ESG research, constructive engagement and, crucially, a long-term approach. Capturing ESG inefficiencies in the European small-cap universe While we believe ESG factors significantly contribute to a company’s competitive advantage and growth, ESG data and ratings are still in an early phase of their development. We believe this creates inefficiencies for active managers to exploit. We think this potential is particularly compelling in a relatively under-researched area such as the European small-cap universe. Numerous vendors currently develop ESG data and ratings for companies. Although these vendors perform a valuable service, each has its own methodology and materiality emphasis, which results in substantial scoring differences even in highly researched markets such as the S&P 500. Figure 1 illustrates this by comparing the ESG scores from two prominent data vendors. If the vendors’ ratings for each company were identical, the dots would form a straight 45-degree plot line from bottom left to top right. However, the dots are significantly scattered, meaning these vendors have very different ESG assessments of the same companies. Figure 1

Anna E. Lundén, CFA Fixed Income Portfolio Manager Equity Portfolio Manager

Louise Kooy-Henckel Investment Director

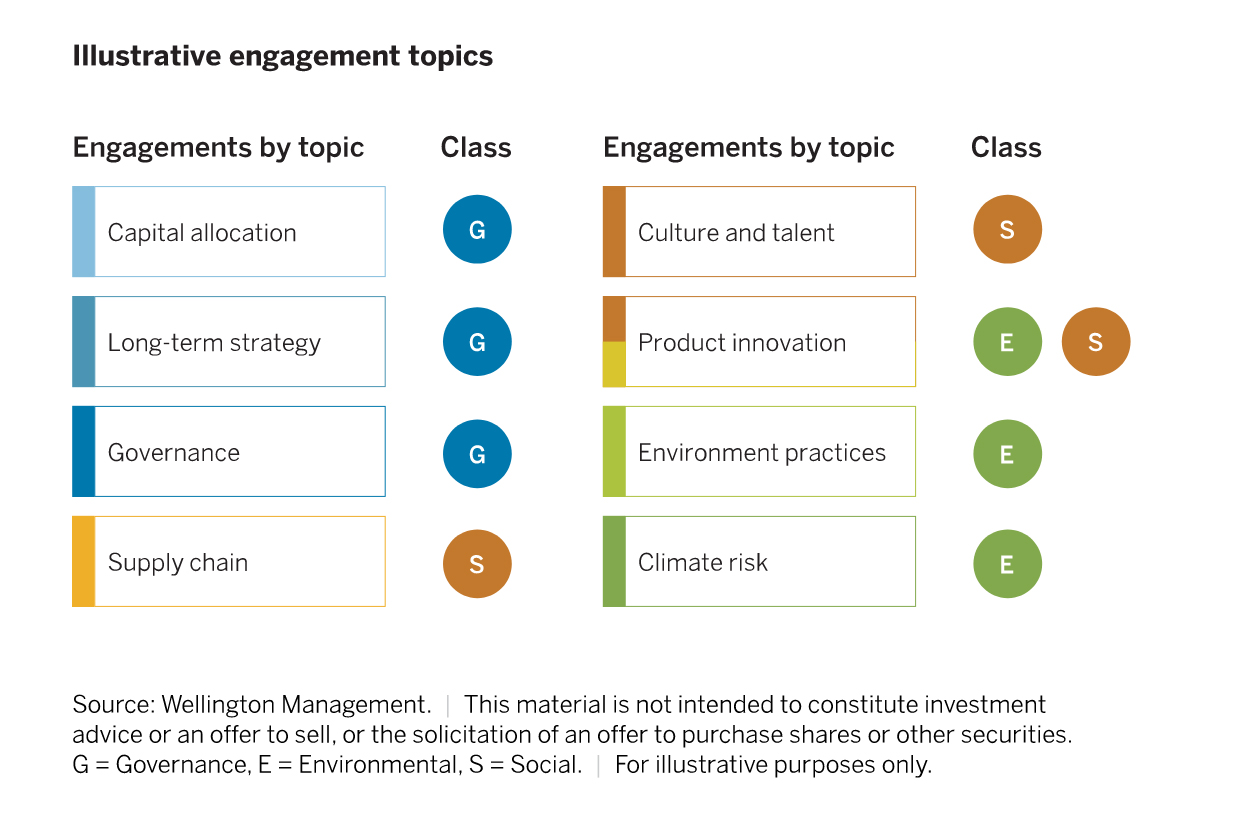

In addition, because third-party ratings are based on disclosures of past activity, they ignore recent or planned improvements. In our view, this challenges their ability to provide a reliable view of a company’s ESG trajectory. Notably, in recent years, the market has driven up the share prices of companies perceived as leaders on ESG, while others with a more promising long-term trajectory may get overlooked. Deep fundamental research of the companies and the ecosystem in which they operate, along with forward-looking ESG assessments of opportunities and risks, can help capture those ESG inefficiencies. We also think it increases the ability for investors to spot sustainable innovation potential ahead of the market. ESG engagement: a source of insight and value creation Proactively engaging with companies on ESG matters and building a constructive long-term partnership may also yield significant insight and, over time, create value. A constructive dialogue can help capture ESG inefficiencies, address ESG misconceptions and support companies on their sustainability journeys. This can be particularly impactful for companies that are still trying to identify and prioritise their material ESG factors. Other companies may already have sound practices, but engagement can help them accelerate their sustainability journey and increase their innovation potential. We do not believe investors should seek perfection; often longer-term outperformance is found in the improvement stories. The key requirement is that the companies are constructive on sustainability and are aligned with our focus on ESG best practices. In Figure 2, we illustrate the key topics we cover in our company meetings and board engagements to try to identify areas of development and improve on these issues. Figure 2

European small-cap equities: sustainable innovation in practice The European small-cap universe encompasses numerous sustainability-conscious companies doing innovative work that potentially enables them to outperform their competition. Below, we outline two company case studies, where we believe in-depth research and engagement has helped uncover significant potential. The first is a UK manufacturer of hard landscaping products. This company has not historically been viewed as an ESG leader by the market as it is a high carbon-emitting sector and relatively high emitter for our universe. In reality, it has a very thoughtful and innovative approach to ESG and sustainability. • This unexpected ESG leader has a long-standing agenda on all aspects of ESG, and an increasing percentage of its research and development budget has been channelled towards sustainable and environmentally conscious projects. • The company manufactures innovative anti-flooding products, provides product-level carbon-data, which is unique in the industry, and has even developed a carbon-neutral process for manufacturing concrete bricks. • Its offering helps customers to manage their environmental impact, reduce their carbon emissions and make informed product decisions. In addition, it reports full CO2 emission data on large-scale construction projects. The second example is a Scandinavian producer of biochemicals. Again, the market and existing ESG metrics have failed to capture the significant strides this company has made in relation to ESG and sustainability. • For more than a decade, this company has evolved from a relatively cyclical business with a narrow end- market exposure to one that has a diverse and expanding range of new applications, all requiring natural raw materials. • Using every component of its raw material — wood — and the expertise of its R&D and technical sales team, the company enables customers to replace oil-based products and ingredients with sustainable alternatives. Thanks to its innovations, wood-derived ingredients are now prevalent in everything from concrete admixtures and plant protection to animal feed, electric car batteries and even toothpaste. To find out more about our approach to sustainable investing click here

Green and grounded

As the need to fight climate change takes root, we talk to fund managers about the pros and cons of making their travel itineraries less carbon-intensive ‘In 2019, I clocked up 220,000 air miles – with one airline. I don’t see anyone ever going back to those levels.’ Those were the words of a senior investment manager who was visiting London from New York at the start of September. This marked his first foreign trip since March 2020 and he admitted to finding it more gruelling than he had previously recalled. The fund manager, who will remain anonymous, said there are two reasons his previous frequent flyer tally will not be matched – personal preference and, perhaps more tellingly, environmental concerns. In terms of once treating the airport lounge as a second home, this manager was far from alone. Fund management is, after all, a global business and, pre-2020, the job entailed many short- and long-haul journeys to meet companies or prospective clients. Another fund manager once joked about having flown from the firm’s London base to Australia to conduct a single pitch to one of the country’s giant superannuation funds. This wasn’t some 1980s City-of-London excess but something that was viewed as fairly familiar, even in the mid-2010s. However, as Covid-19 struck, skies grew suddenly quieter or even silent. Grounded planes and shuttered airports forced people online and the asset management industry went from zig-zagging across the planet in planes to pinging across virtual networks via video conferencing. The decline in air traffic was held up as an improvement for air quality and overall climate impacts. However, many reports, including a COP26-sponsored study into long-term aviation trends published in July 2021, said this was only ever likely to be a temporary stop: https://www.nature.com/articles/s41467-021-24091-y#Sec2 ‘The changes in 2020 due to Covid-19, as dramatic as they are for individuals and the global economy, only have a minor effect on the overall climate impact of aviation as long as a recovery follows. From the experience of other crises (e.g. SARS, 9-11, etc.) we might expect a fast recovery,’ the authors wrote.

Chris Sloley Editor, Citywire Selector

Jonathan Curtis, Franklin Templeton

‘I can speak to you in London from here in San Francisco, then I can log onto a call with my colleagues in New York and then tomorrow be up to talk to businesses in Asia’

Virtual air miles However, as the march towards normalisation gathers pace, more fund managers are back in the boarding queues and embarking on the whistlestop tours of yesteryear. On the other hand, advances in virtual meetings technology mean there is likely to be a concerted drop-off in such intensive tours of duty and some marginal environmental gains. Companies, such as Amundi, have outlined plans to limit company-wide travel to the bare necessities, as a huge amount of the workload can now be done virtually. Jonathan Curtis, a tech manager at Franklin Templeton, exemplified the ‘new normal’ during a discussion with Citywire Selector last year. ‘I can speak to you in London from here in San Francisco, then I can log onto a call with my colleagues in New York and then tomorrow be up to talk to businesses in Asia,’ he said. ‘Before, that would be several flights, time at airports and also then the catch-up on the work that I may have missed because of the time taken travelling.’ But, anecdotally, many fund managers said they enjoyed being back on the road, visiting both clients and companies, as there is more to be gathered from a face-to-face interaction than can sometimes be gained from more-curated video calls. The long-ingrained need to go and ‘kick the tires’, is often important for building relationships but can also add an important governance element, as fund managers get a better understanding of the actual people they are dealing with. The car’s the star So, what can fund managers do if travel remains such a crucial element? Some have taken the challenge in new directions and equity income investor Ben Peters of Evenlode is among those, quite literally, driving change. He spoke to Citywire Selector from behind the wheel of his Tesla while partway through returning from a 10-day fact-finding mission around continental Europe. ‘Travel is the most carbon-intense thing we do as a company, beyond heating our London offices. Personally, I want to reduce my emissions and I am very invested in decarbonisation,’ he said. ‘But, if you want to see important change then you have to get out there and do it. I have clients and prospective clients in Zurich, so I thought why not go to them – why not drive?’ Peters, who co-runs the Evenlode Global Dividend and Global Income funds with Chris Elliott, plotted a course that would take him through existing and potential clients and companies across France, Germany, Belgium and Switzerland to maximise the efficiency of the trip. ‘I have driven around Europe recreationally, on holidays and such, so I thought it was a logical step. I also find that when you go to these places, they are much more open and appreciative of your time.

Ben Peters, Evenlode

‘If you want to see important change then you have to get out there and do it. I have clients and prospective clients in Zurich, so I thought why not go to them – why not drive [rather than fly]?’

‘There is a cultural element that you can only find by going there. It is an intangible aspect but it does feed into the governance aspect of what we do.’ There are promising elements to the boom in digital conferencing, but Peters believes that physical person-to-person element is hard to replicate online. ‘We will likely get there but in a 30-minute or one-hour call with a new prospect, you wouldn’t get the same sense of a place you would get just from being in their offices or seeing what hierarchy or structure dictates where the team sit at their desks, for example.’ Listen up One question Peters said he fields a lot is how do you fill the ‘dead time’, while driving? His counterparts on planes or in airport lounges have the luxury of being able to work or read during the flight, whereas he has to concentrate on the road. ‘It is different for everyone but I take in a lot of information aurally. So I listen to news podcasts or earnings calls or other information that has been put in an audio format. Of course, I need to concentrate on the road, but I feel there is a lot of information I can still gather while thinking and driving.’ Peters understands not everyone can afford a 10-day trip, especially when a short flight is an alternative, but the carbon intensity of an electric vehicle compared with a plane is significantly lower. However, again, Peters is aware of limitations. ‘Connectivity can be an issue, if you are driving through a signal blackspot, but there are other limitations too,’ he said. ‘For one, I have driven through four countries and even though charging is not a major issue, the German power grid is largely coal-based. So I am effectively charging an EV with coal energy, which seems counterintuitive. ‘I think we will move in the right direction though, and as the German government witnesses a growth in EV use then we are likely to see a response in terms of how those networks themselves are powered. It is a long-term challenge but it is an important one.’

Statements like these are meaningless without context. First, let me explain what we mean by net-zero. This means investing in companies that emit zero carbon dioxide on a net basis by 2050 at the latest. Here is some more context. In 2015, the Paris Agreement was signed by 192 countries, which was unprecedented [1]. The goal was to limit the rise in temperature to below 2°C above preindustrial levels, plus pursue efforts to limit a temperature increase to 1.5°C. Limiting the rise in temperature is essential for the future of humanity. It is also not just important for society but for the long-term returns of investment portfolios. Protecting investors against climate change If you are a millennial or younger, a 2050 target date to reach net-zero makes sense. Many people in this age cohort expect to retire after this date. The risk these investors face is that they might not be able to retire if climate change jeopardizes the performance of their pension portfolios. Moreover, there is a risk that they would retire in a world where the quality of life has rapidly declined due to climate change. Markets do not fully price in climate risk so far ahead because the timing of the potential impact is difficult to pinpoint. The complexity of the topic makes it challenging for the average investor to act upon it today. Progress has been made, however, through improved reporting on the impact of climate change on investments. For instance, the Task Force on Climate-Related Financial Disclosures (TCFD) has set standards for companies to provide clear, comprehensive, and high-quality information on the impact of climate change. Making this disclosure mandatory is increasingly being discussed by regulatory authorities. In some countries like the UK, it is already mandatory. Beyond regulations and reporting, we also need to help investors achieve their goals by offering guidance. We should do this no matter how long their time horizon or how complex the topic is. By building portfolios that manage climate risks and by investing in solutions for the energy transition, we can help serve investors better. This approach can help deliver returns that are attractive, sustainable, and long-term, plus support the transition to a net-zero society. Take an active ownership approach to climate risk It is also important to realize that as an investor you are the partial owner of a company. This ownership should also be used to support and influence the companies we invest in. This includes actively engaging with companies to ensure that they commit to the net-zero transition and incorporate climate risk in their business and strategies. Engaging as an active owner can therefore have a positive impact on society as well as on the companies we invest in, which should in turn support long-term financial returns. Make attractive financial returns while having a positive impact on society Ultimately, considering the risks and opportunities from climate change makes sense, both from a financial and societal perspective. Integrating climate aspects in portfolios improves resilience to climate risk and offers potential opportunities stemming from the transition. This benefits both society and long-term investment returns. Therefore, it is an investment approach that will become even more important in the future as a greater number of investors around the world adopt it. This is about being ready for the future when it comes and reducing the exposure our investors have to climate risk. Climate change is one of the key risks we face in our lifetime. The transition to a net-zero society will be one of the most important trends of the next few decades. Making sure investment portfolios are ready is critical. The transition to net-zero can be a win-win for both investors and society. That is why we are committed to it!

Let’s get our portfolios to net-zero by 2050

Jeroen Bos Global Head of Sustainable Investing at Credit Suisse Asset Management

Tara Stilwell, CFA Equity Portfolio Manager

[1] United Nations. (n.d.). The Paris Agreement. Retrieved May 25, 2022, from https://www.un.org/en/climatechange/paris-agreement.

How getting to net-zero by 2050 might work Climate risks and opportunities can be integrated into portfolios in different ways. First, it is important to assess how prepared companies are in dealing with the impact of climate change. For instance, how exposed is a company to the impact of floods, droughts, or extreme weather caused by climate change? Second, it is important to assess how well a company can cope with the disruptive nature of the energy transition. You need to assess the resilience of its business model and products, and whether its products are at risk of being displaced. The preparations a company makes demonstrate its commitment to achieving net-zero. Offering a clear strategy or commitment to reaching net-zero is a good sign. Evidence that they are using science-based targets to see how quickly they need to reduce emissions to meet their goals is even better. The climate transition also brings opportunities for investors. Therefore, it is important to assess which companies will benefit from the net-zero transition and where the greatest potential could exist. Companies that are ill-prepared for climate risk should be approached with caution when investing. These companies are likely to suffer the most if there is a climate shock event. Their revenues and profits could be hit hard, hurting overall portfolio performance. This is exactly what investors should avoid while also focusing more on investing in the likely winners of the net-zero transition.

Jeroen Bos has served as Global Head of Sustainable Investing at Credit Suisse Asset Management since January 2022. He also sits on the Sustainability Leadership Committee of Credit Suisse Group. Before joining Credit Suisse, Jeroen spent 14 years with NN Investment Partners (NNIP). Prior to that, he held senior positions at UBS in New York and JP Morgan in London. In addition, Jeroen is a member of the investment committee of the Rail & Public Transport Pension Fund in the Netherlands. Jeroen holds a master’s degree in Economics from the Vrije Universiteit Amsterdam (VU). He is also a Chartered Financial Analyst (CFA) and holds multiple certifications.

Disclaimer/Important information This material constitutes marketing material of Credit Suisse Group AG and/or its affiliates (hereafter “CS”) and provides information on a strategy. This material does not constitute or form part of an offer or invitation to issue or sell, or of a solicitation of an offer to subscribe or buy, any securities or other financial instruments, or enter into any other financial transaction, nor does it constitute an inducement or incitement to participate in any product, offering or investment. Nothing in this material constitutes investment research or investment advice and may not be relied upon. It is not tailored to your individual circumstances, or otherwise constitutes a personal recommendation, and is not sufficient to take an investment decision. The information and views expressed herein are those of CS or guest commentators at the time of writing and are subject to change at any time without notice. They are derived from sources believed to be reliable. CS provides no guarantee with regard to the content and completeness of the information and where legally possible does not accept any liability for losses that might arise from making use of the information. If nothing is indicated to the contrary, all figures are unaudited. The information provided herein is for the exclusive use of the recipient. The information provided in this material may change after the date of this material without notice and CS has no obligation to update the information. This material may contain information that is licensed and/or protected under intellectual property rights of the licensors and property right holders. Nothing in this material shall be construed to impose any liability on the licensors or property right holders. Unauthorised copying of the information of the licensors or property right holders is strictly prohibited. This material may not be forwarded or distributed to any other person and may not be reproduced. Any forwarding, distribution or reproduction is unauthorized and may result in a violation of the U.S. Securities Act of 1933, as amended (the “Securities Act”). The securities referred to herein have not been, and will not be, registered under the Securities Act, or the securities laws of any states of the United States and, subject to certain exceptions, the securities may not be offered, pledged, sold or otherwise transferred within the United States or to, or for the benefit or account of, U.S. persons. In addition, there may be conflicts of interest with regards to the investment. In connection with the provision of services, Credit Suisse AG and/or its affiliates may pay third parties or receive from third parties, as part of their fee or otherwise, a one-time or recurring fee (e.g., issuing commissions, placement commissions or trailer fees). Prospective investors should independently and carefully assess (with their tax, legal and financial advisers) the specific risks described in available materials, and applicable legal, regulatory, credit, tax and accounting consequences prior to making any investment decision. Copyright © 2022 CREDIT SUISSE GROUP AG and/or its affiliates. All rights reserved.

Venture capital firms falling behind on ESG

Responsible Investment in Venture Capital report UNPRI

‘Venture capital GPs must do more to consider the environmental outcomes their startup companies might shape once they achieve scale’

Lack of resources and influence One of the problems highlighted by the report is that few VC managers have dedicated ESG professionals, and when there are teams, they are generally small and have limited resources. Also, as minority investors, VC managers do not have as much influence over company decisions as a majority investor might. The problem of influence extends beyond the relationship between the fund manager and the portfolio company. Investors in VC funds do not have as much power to push the managers into greater ESG adoption. ‘The venture capital industry does not have a strong culture of client – or public – disclosure, with firms regulating the flow of information very tightly. This is not just ESG related – for example, one GP explained that they only report fund-level investment performance to LPs, rather than disclosing the performance of individual holdings. Venture capital GPs that collect ESG data do not always report it to LPs, making it difficult to monitor and engage on those risks,’ the report said. There are some positives, however. Although in the US, ESG is still seen as a box-ticking exercise, there is growing interest in incorporation in Europe, the report found.